By: Matt @ Home & Pocket

May 12, 2025

Introduction

In today’s world of rising prices and societal pressure to “keep up,” the idea that a single-income household—especially one with children—can thrive may seem like a pipe dream.

But the truth is, many American families can live comfortably, save for retirement, and even build wealth on one middle to upper-middle-class income.

The catch? It requires a mindset shift.

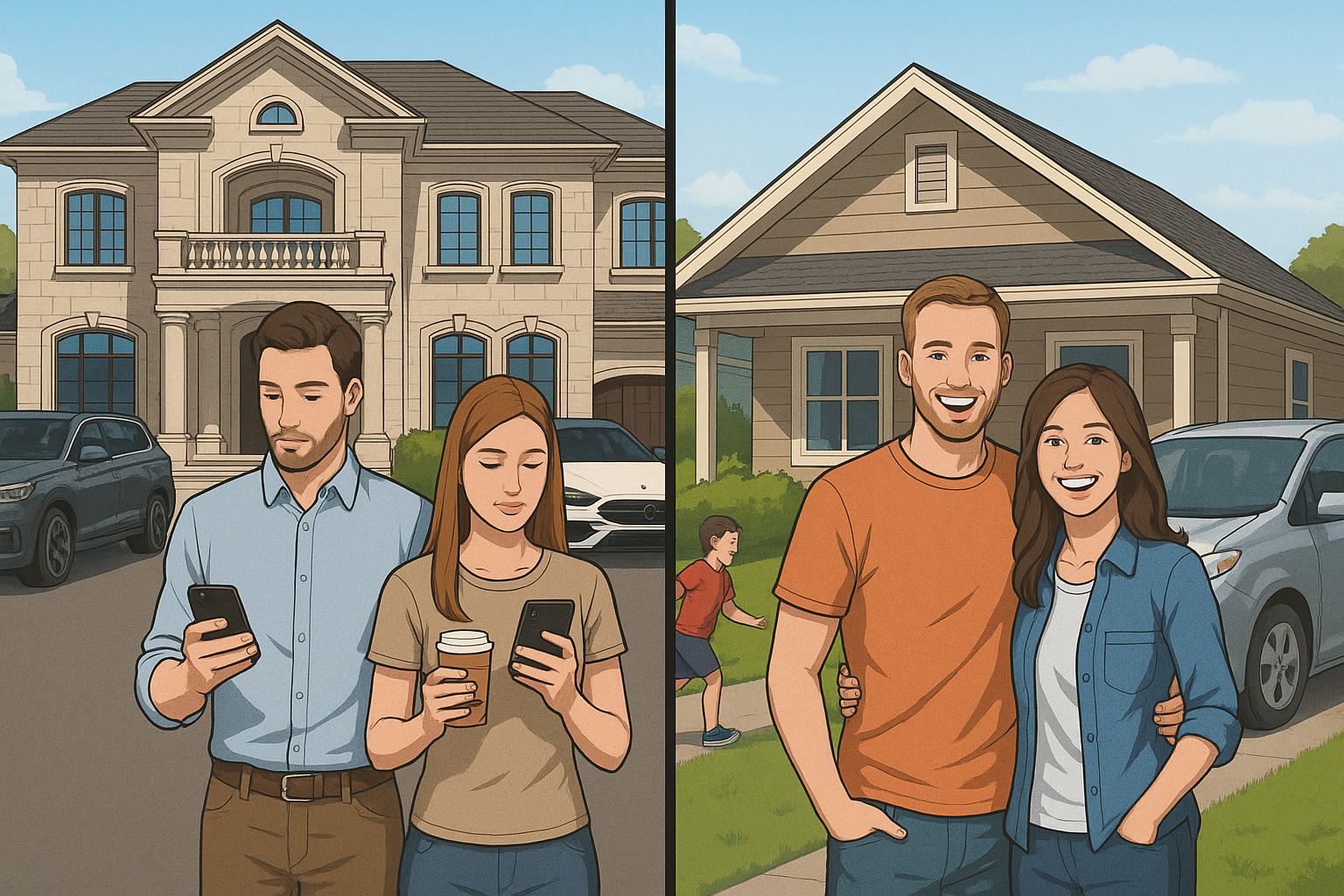

We’ve been sold a lifestyle built around materialism: newer, bigger, flashier. We’re told success looks like a $70,000 SUV, a 3,500-square-foot house, $6 lattes, and three international vacations a year.

But none of those things are necessities. In fact, they’re often barriers to long-term financial freedom.

This article explains how families of four or five can succeed on one solid income.

They do this by making smart, intentional choices. These choices prioritize financial stability over social status.

I’ve been supporting a single-income household for nearly a decade now, with a wife and three kids — and it’s been an incredible experience.

The time spent together as a family, and the fact that our children are being raised by their mother instead of strangers at daycare, are blessings we deeply appreciate.

These are values we, as Americans, should begin to prioritize once again.

What Is a Middle to Upper-Middle Class Income?

Before diving in, let’s define the income range. A “middle to upper-middle-class” household income in the U.S. varies by location, but generally falls between $70,000 and $150,000 annually.

In many states, particularly in the South and Midwest, this is more than enough for a family to live well—especially if it’s managed wisely.

The Illusion of “Normal” Spending

Modern American spending habits have normalized the extraordinary.

What used to be luxuries—like new cars every few years—are now seen as expected. Expansive homes with bonus rooms and ensuite bathrooms for every child are expected too.

Even weekly restaurant meals are considered normal now.

Let’s break down some of the most common budget-busters:

1. Cars: The $800-a-Month Mistake

The average new car payment in 2024 is over $750/month—per vehicle. For two working parents, it’s common to see families with $1,500/month in car payments, not including insurance, fuel, and maintenance.

Here’s the truth: modern cars are incredibly reliable. A well-maintained used Toyota, Honda, or Ford can last 200,000+ miles. That’s 10–15 years of life.

Alternative approach:

- Buy used (3–6 years old).

- Pay in cash or finance only what you can afford to pay off quickly.

- Keep the car for 10 years.

A reliable used car at $12,000–$15,000 can serve your family just as well as a new $45,000 SUV—without bleeding your monthly income.

2. Homes: Bigger Isn’t Better

The American Dream once meant owning a modest home with a yard.

Today, we’re pitched custom builds with open-concept kitchens, smart everything, and premium finishes.

But bigger homes mean bigger mortgages, bigger utility bills, and more upkeep. And in many cases, space goes unused.

Strategy for the one-income family:

- Buy below your means.

- Consider an older home in a safe neighborhood.

- Embrace DIY projects over time.

- Focus on functionality over aesthetics.

A smaller home with a paid-off mortgage is far more freeing than a luxurious one that eats up 40–50% of your income.

Related Reads:

Reduce Your Expenses: 3 Areas Families Overspend

5 Essential Steps for First-Time Home Buyers

Strengthen Your Marriage with Financial Communication

Top 15 States for Young Couples to Raise a Family: Where to Find the Right “Stuff” for Your Future

3. Dining Out and Coffee Shops

Grabbing food after a long day is tempting—especially for parents. But eating out 2–3 times a week can cost $300–$500 a month, and coffee runs add up fast.

A family of five eating out even once a week could easily spend $200–$300 per month. That’s $2,400–$3,600 a year—just on convenience.

Better habit:

- Meal prep simple dinners.

- Invest in a quality coffee maker or espresso machine.

- Save restaurants for special occasions.

This one switch can save thousands per year.

4. Expensive Hobbies and Vacations

There’s nothing wrong with enjoying life—but expensive hobbies (boats, ATVs, golf memberships) and lavish vacations often do more damage than good.

A single week at Disney or abroad can cost $5,000–$10,000.

Instead:

- Choose road trips and national parks.

- Visit family or explore nearby attractions.

- Prioritize simple experiences over Instagram-worthy ones.

You can still create incredible family memories—without the five-figure price tag.

5. Subscription Overload

Netflix, Disney+, Amazon Prime, Spotify, Apple Music, meal kits, beauty boxes—these small monthly payments add up.

The average American household now spends over $200/month on subscriptions.

That’s $2,400 per year that could go toward:

- A Roth IRA.

- A family emergency fund.

- Kids’ 529 college savings accounts.

Trim the fat and reclaim that cash.

A Realistic One-Income Budget Breakdown

Let’s say a family of five lives on $100,000/year before taxes.

After taxes (federal, state, FICA), that’s roughly $75,000–$80,000/year net—or about $6,250/month.

Here’s a sustainable monthly breakdown:

| Category | Monthly Budget |

|---|---|

| Mortgage/Rent | $1,500–$1,800 |

| Utilities & Internet | $300 |

| Groceries | $800–$1,000 |

| Transportation (1 car) | $400–$600 |

| Health Insurance | $500–$800 |

| Childcare/School Needs | $200 |

| Entertainment & Dining | $200 |

| Subscriptions | $50 |

| Miscellaneous | $200 |

| Savings & Retirement | $1,000–$1,500 |

With careful management, there’s still room for flexibility and saving—and that’s the key.

Benefits of the One-Income Life

Besides financial simplicity, a one-income household offers some underrated advantages:

- Less stress juggling careers and childcare.

- More quality time with kids.

- Easier coordination of schedules, appointments, and home life.

- Greater focus on long-term planning and values.

When both parents work, the net financial gain is often less than people think once you factor in:

- Childcare

- Extra commuting

- Eating out

- Professional wardrobe

- Second car expenses

Often, one solid income—managed wisely—yields nearly the same bottom line with far more lifestyle control.

Building Wealth on One Income

You don’t need two high salaries to build wealth. You need three things:

- Discipline

- Consistency

- Time

A family saving and investing $1,000/month can build:

- $500,000 in 20 years (assuming 7% annual returns)

- Over $1 million in 30 years

That’s without ever earning more. The power is in living below your means and letting compound interest do the work.

Cultural Shift: Redefining Success

American culture glorifies the appearance of wealth more than actual financial stability.

We compare ourselves to the neighbors with the pool, the new truck, and the remodeled kitchen—not realizing they may be living paycheck to paycheck.

What if we changed the definition of success to:

- Being debt-free?

- Having time with family?

- Funding your kids’ education?

- Retiring early or traveling in your 60s?

Living on one income forces intentionality—but that’s where real freedom begins.

Final Thoughts

Can a family of four or five make it on one income in America today?

Absolutely. But not if they’re trying to live the Instagram version of life.

If you’re willing to trade convenience for savings, image for substance, and short-term splurges for long-term security, one income is not only enough—it can be more than enough.

In a world that’s constantly shouting “more,” choosing “enough” is a powerful financial move.

Leave a Reply